Is ‘affordable’ housing in Sub-Saharan Africa being appropriately addressed?

Is the current supply of ‘affordable’ housing within Sub-Saharan Africa appropriately addressing the housing deficit?

As part of JLL’s commitment to improving transparency in Sub-Saharan African (“SSA”) real estate markets, JLL’s Strategic Consulting team has been investigating the status of the affordable housing sector in the region. The issue of housing affordability is a source of concern for most countries across the African continent. Given the current pace of population and urbanisation growth, the shortage of housing is expected to increase dramatically in the coming decades, potentially entailing a barrage of social and economic problems. While our intent is to cover the whole Sub-Saharan African region, the countries upon which we have focused our analysis are primarily South Africa, Kenya, Nigeria, Ghana and Tanzania. The key findings from our research will be published on social media. This second article aims to provide an overview of the housing deficit within Sub-Saharan Africa, in addition to exploring whether affordable housing really is affordable.

According to the Centre for Affordable Housing Finance in Africa (CAHF) in 2016, a substantial housing deficit exists within Sub-Saharan Africa: South Africa (2.3 million units), Kenya (250,000 units annually), Nigeria (17 million units), Ghana (1.7 million units) and Tanzania (3 million units).

In light of the apparent housing deficit, many countries have dedicated a substantial portion of their efforts to breaching the gap within the affordable housing market. Such efforts have been outlined in their various national vision plans, namely: National Development Plan: Vision for 2030 (South Africa), Vision 2030 (Kenya), Nigeria Vision 20: 2020, Vision 2020 (Ghana) and The Tanzania Development Vision 2025.

Supply of affordable housing stock within key cities in SSA

The majority of affordable housing supply within South Africa (SA) is predominantly subsidised by the government and accounts for approximately 30% of the total residential property in the country (CAHF). Within South Africa, there are numerous initiatives aimed at breaching the gap within the affordable housing sector whether it be reduced mortgage initiatives, units available for rental or purchase, development schemes aimed at first time home owners or the provision of government subsidised housing.

In Johannesburg, South Africa, there has been a substantial amount of affordable housing development within the Southern parts of the city. Furthermore, Project Fleurhof (Ext 2) undertaken by Calgro M3, is set to be one of the largest integrated housing developments within the Gauteng region, comprising 9 600 units. On completion, Project Fleurhof will accommodate approximately 83,000 people.

As part of its Vision for 2030, Kenya is to undergo a substantial amount of development over the following years, currently achieving delivery of approximately 50,000 units annually (CAHF). A large portion of this development is to be completed in Nairobi, where the second phase of the Urban Renewal project is to comprise of 100,000 units within the Eastlands area. Other low cost housing initiatives in the country are implemented on a much smaller scale with some developments comprising just 150 units. A unique approach in breaching the housing gap within the market, one of Urbanis Africa’s projects involves the sale of plots of land to low-income households, where they are then able to engage with the buyers in a construction programme.

The supply of affordable housing within Nigeria is unable to keep up with the rapid growth and urbanisation of the population. As a result, the government is encouraging private/public partnerships in an attempt to increase the delivery of suitable housing to the Nigerian population. There are various ongoing schemes within the country with a notable development being Rock City in Abuja. The project is to comprise of 10,000 units upon completion, with the first phase of 5,000 units already complete. CAHF estimates that approximately 100,000 units are brought onto the Nigerian market each year.

In Ghana, the majority of affordable housing development is undertaken in the Greater Accra Region, Kumasi and Takoradi with approximately 90% of the supply being provided by small, local contractors. According to the CAHF, approximately 40,000 units are being brought onto the market annually.

In line with the Tanzania Development Vision 2025, the Tanzania Public Servants Housing Scheme (PSHS) which launched in 2015, is envisioned to comprise 50,000 units by 2020 with three of the thirteen anticipated projects taking place in Dar es Salaam. However, at the end of 2016, only 700 of these units have been completed.

Existing price points of current supply

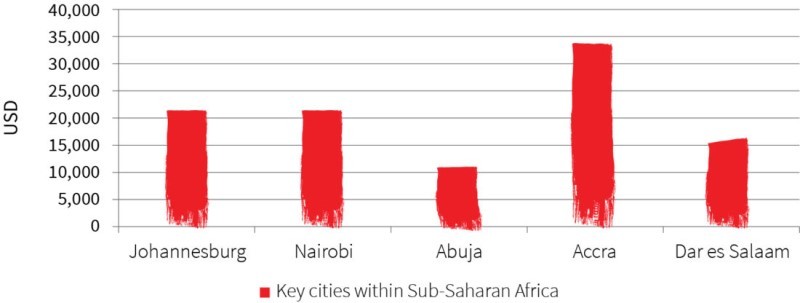

The graph below represents the average prices of two bedroom affordable housing units as per data gathered by JLL.

When assessing the price points of current supply, it is crucial to understand whether this supply is able to meet the current demand and whether or not that translates into affordable housing for those in need of it. An assessment on such affordability is discussed below.

Is affordable housing actually affordable in SSA?

The table below presents the forecasted income distribution of households within the cities under review in 2017, as per Oxford Economics data:

Assuming that 30% of households’ income could be used as a relatively standard measure in calculating their capacity to repay a mortgage, it is estimated that households with the possibility of purchasing affordable housing units within each of the cities under study, are those highlighted in yellow above.

Consequently, based on the average price points of supply as previously indicated, it is estimated that 60% of households within Johannesburg are unable to afford an affordable housing unit within the city. Furthermore, the portion of total households unable to afford an affordable housing unit within the remaining cities are as follows: Nairobi (51%), Abuja (12%), Accra (75%) and Dar es Salaam (85%).

It is worth noting that the majority of the population in four out of the five cities are unable to afford such units. Furthermore, only 25% of households within Accra and a mere 15% of households in Dar es Salaam are able to afford these units.

It is for this reason that we are able to deduce that the majority of current supply of affordable housing within Sub-Saharan Africa does not meet the needs of the population in demand and is not ‘affordable’ as such. It is ironic that the provision of such housing is labelled as ‘affordable’ when the majority of the population within the cities under study are unable to afford such a unit.

Although efforts are being made to address the housing deficits within the various countries, it seems that there is a misalignment in the priority ranking of this issue, judging by the size of the gap in the need and delivery. Perhaps alternative measures are required in order to accurately address this problem.

In our subsequent article, we investigate technologies which are to bring down the construction costs of affordable housing in the hope of further breaching the gap within the market.